A naukri.com initiative

Medium

3w

65

Image Credit: Medium

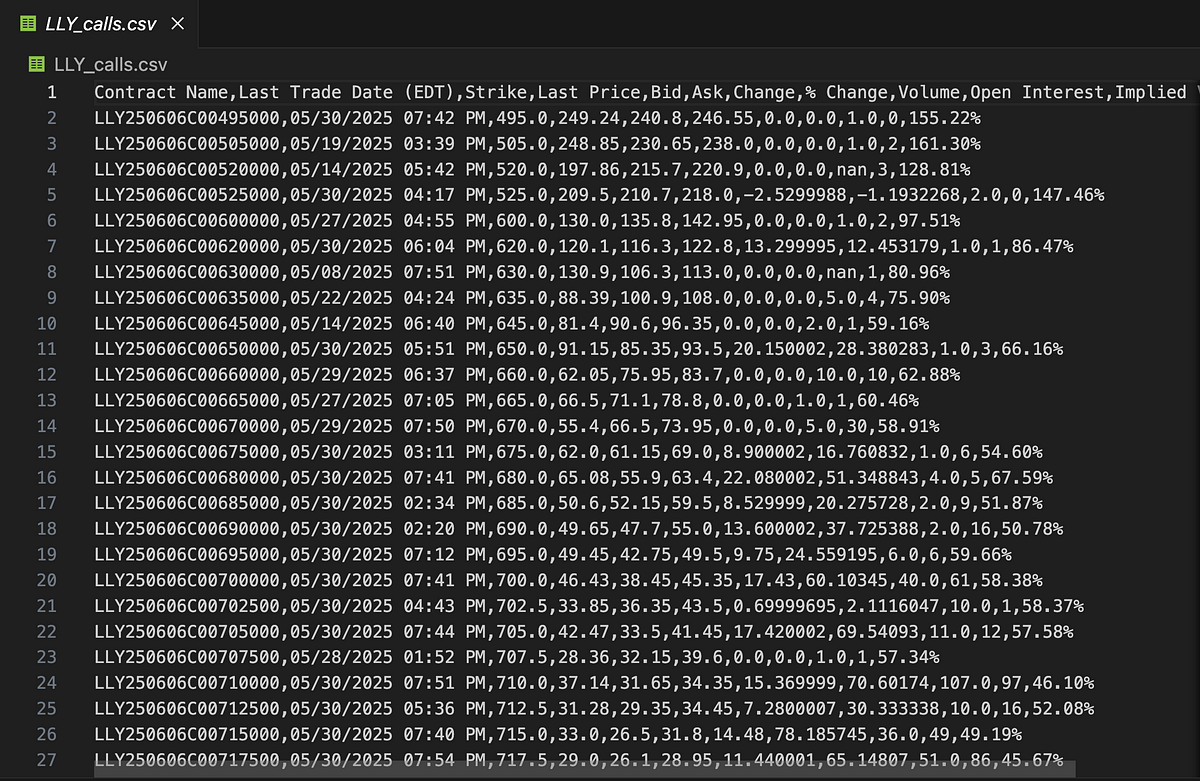

Pulling Options Data with Python and yFinance — and Saving it Like a Pro

- The goal of the code is to retrieve options data for a specific stock ticker and expiration date using the yfinance library in Python.

- The code formats the options chain data neatly and saves the data into two CSV files:

_calls.csv and _puts.csv. - Each row in the CSV files includes details such as contract symbol, last trade timestamp, strike price, bid/ask prices, volume, open interest, implied volatility, among others.

- This script can be useful for options backtesting, volatility screening, and automated reporting by leveraging real-time options data and Python's capabilities.

Read Full Article

3 Likes

For uninterrupted reading, download the app