A naukri.com initiative

Medium

1M

94

Image Credit: Medium

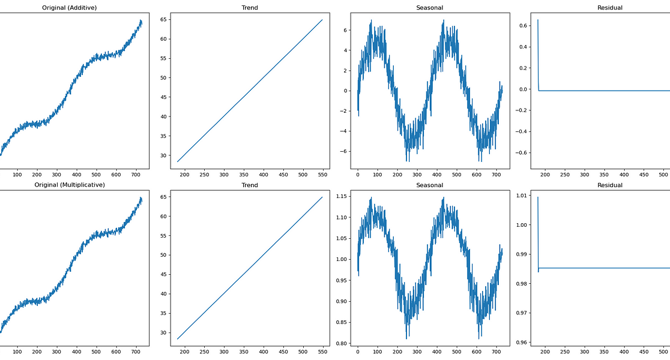

Seasonal and Trend Decomposition Methods for Time Series Forecasting

- Time series decomposition is based on the idea that time series can be broken down into four fundamental components: trend, seasonality, cyclical patterns, and random variations.

- Classical decomposition provides valuable insights, but modern techniques like the STL method offer more flexibility and robustness in handling seasonal components.

- Decomposition results provide actionable insights about trend direction, trend strength, seasonal amplitude, and residual variance.

- Seasonal and trend decomposition methods are essential for understanding time series data and can inform forecasting, anomaly detection, and pattern analysis.

Read Full Article

5 Likes

For uninterrupted reading, download the app