A naukri.com initiative

Medium

1d

129

Image Credit: Medium

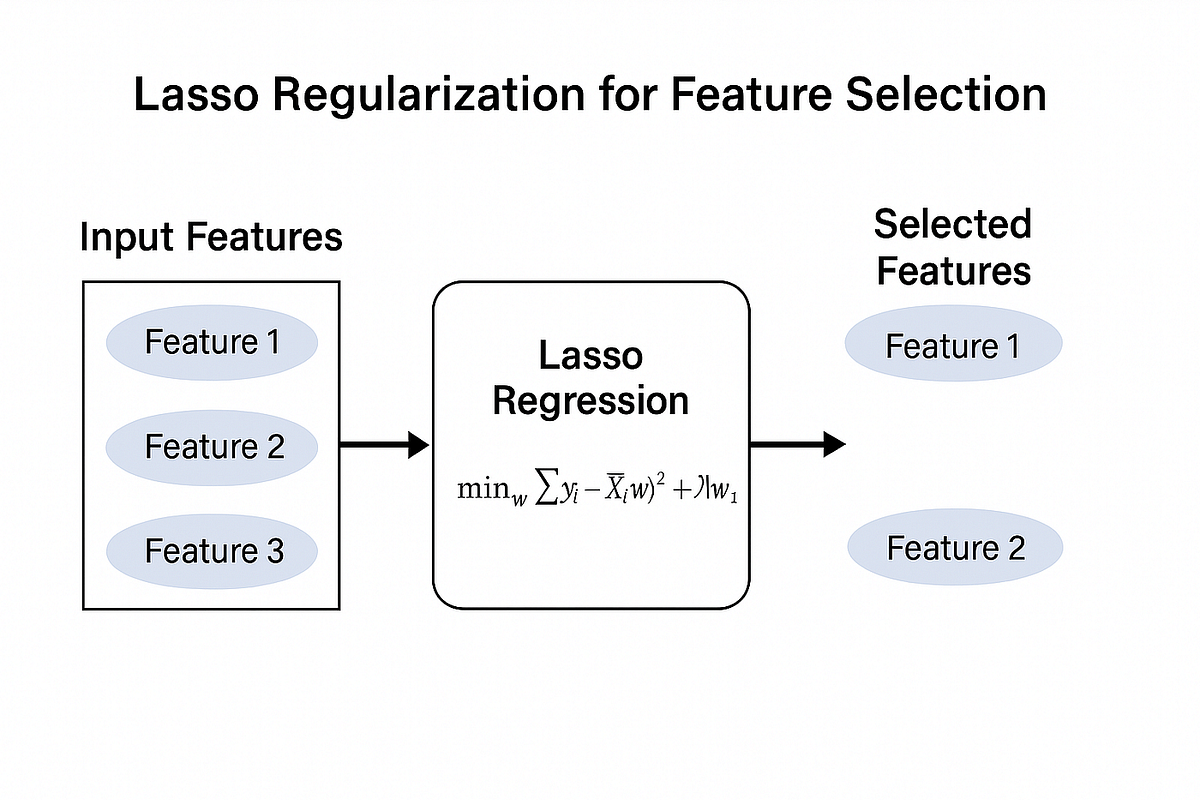

Understanding the Magic of LASSO Feature Selection

- LASSO is a technique that combines linear regression with L1 regularization to automatically select relevant features and produce sparse models.

- The optimization function of LASSO minimizes the sum of squared residuals while constraining the sum of absolute weights, forcing many coefficients to zero.

- L1 regularization in LASSO creates a constraint region in parameter space, essential for feature selection by forcing some coefficients to exactly zero.

- LASSO is useful for feature importance analysis, robust to multicollinearity, and can be visualized through the regularization path of coefficients.

Read Full Article

7 Likes

For uninterrupted reading, download the app